Benefits of infrastructure investing

- Fri 05 June 2020

Reliable yield, predictable returns, and inflation protection are long-term characteristics of the sector.

Demand for infrastructure assets has grown exponentially in recent years. Because of the unique way essential services assets provide for society, investors can access a strongly differentiated set of financial characteristics compared to other asset classes.

Examples of infrastructure assets include energy, utilities, airports, toll roads and communication towers.

(Editor's note: Do not read the following ideas as a sector recommendation. Do further research of your own or talk to a licensed financial adviser before acting on themes in this article).

Many investors are particularly drawn to the attractive yield and inflation protection these assets can provide. Because infrastructure assets often have their profits guaranteed by long-term contracts or regulation, returns tend to be relatively predictable over the long term.

Additionally, these assets can provide a natural hedge against rising inflation through:

- Long-term concessions with inflation-linked increases.

- Regulation that allows a real return to be earned.

- Pricing power due to the monopolistic characteristics of the industry and its high barriers to entry.

For investors, this provides extremely good visibility for cash flows and ultimately a sustainable income stream.

Two ways investors can access infrastructure is through unlisted and listed infrastructure funds. At a high level, the assets in unlisted infrastructure funds are held privately rather than listed on a sharemarket, while listed infrastructure funds invest in infrastructure companies’ securities.

Figure 1: How listed and unlisted infrastructure differs

Listed | Unlisted | |

|---|---|---|

Geographic and asset diversity | Very high | Low |

Liquidity | Very high | Low |

Daily valuations | Yes | No |

Volatility of valuation | High | Very low |

Control | Low | Low to very high |

Transaction cost | Low | High |

Investment horizon | Medium term (~5 years) | Long term (~10 years) |

Source: AMP

Alongside this demand growth for infrastructure assets by investors there has been a corresponding increase in undeployed capital within unlisted infrastructure funds.

According to Preqin, “dry powder” in unlisted core and core-plus infrastructure has consistently grown from its previous highs to the March 2020 record level of US$122 billion since 2012. Dry powder is committed capital that has yet to be deployed.

It is only natural that listed companies with access to high-quality infrastructure assets have become a viable standalone asset class and are increasingly becoming potential targets for unlisted infrastructure funds under pressure to put capital to work.

Just a decade ago, listed infrastructure was a niche asset class and poorly understood by many investors. It is now a diverse US$3 trillion investment opportunity and more than US$60 billion (source: eVestment, December 2019) is being managed by specialist listed infrastructure managers.

Listed infrastructure expands opportunities

By investing through listed infrastructure, investors can access a broad set of liquid investment opportunities across geographies and sectors that may not be available through direct investment.

Regulatory frameworks and contract structures vary greatly from sector to sector and from region to region, as they are based on and exposed to macro variables in different ways.

Furthermore, diversification can help mitigate risk in concentrated exposure to regional economic downturns and regulations.

Although listed and unlisted infrastructure assets with the same economic exposures will behave similarly to changes in the economic environment, valuation leads and lags do arise between both unlisted and listed infrastructure, due to the mark-to-model versus mark-to-market effect.

Unlisted infrastructure assets’ valuation cycles are typically bi-annual with fewer unlisted comparative transactions, resulting in lower volatility. While daily valuations can lead to higher volatility for listed infrastructure, active listed infrastructure managers are able to take advantage of the opportunities it can create.

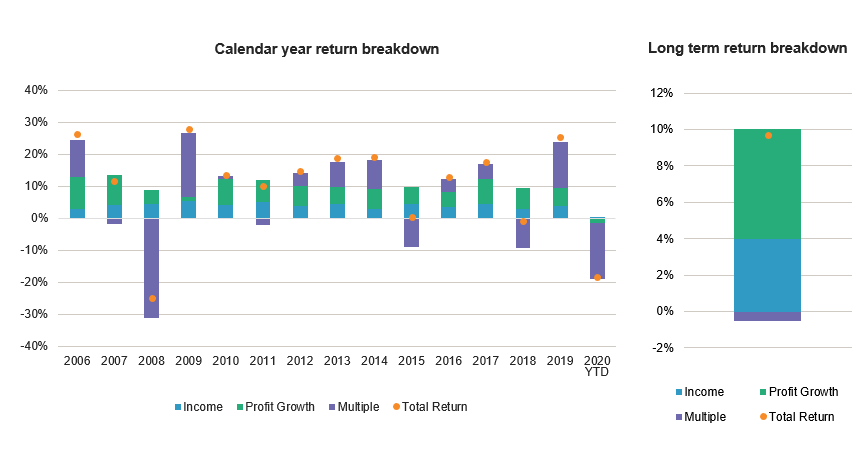

Despite volatility of valuation, long-term infrastructure investors should appreciate the majority of the volatility is driven by multiple expansion/contraction, but over the long term this has little impact, as cash flow growth is ultimately what delivers returns.

Years with negative total return have primarily been driven by (valuation) multiple compression, but over the long term the multiples effect has been neutral. This is why we believe it is key to focus on cash flows and that short-term volatility can create opportunities.

Figure 2: Listed infrastructure return breakdown

Source: AMP Capital, Bloomberg. Data from 31 December 2007 to 31 March 2020. Data frequency: quarterly. Data period: Q1 2006 to Q1 2020. Currency: local. Past performance is not a reliable indicator of future performance.

Due to its defensive attributes, listed infrastructure has historically provided investors a greater level of downside protection when compared to broader global equities.

As can be seen in the table below, the asset class has historically delivered superior returns with lower volatility compared to global equities.

Figure 3: Listed infrastructure versus global equities

| Listed Infrastructure | Global equities |

|---|---|---|

Total Return | 9.7% | 4.9% |

of which dividends | 4.0% | 2.1% |

of which growth | 6.1% | 2.6% |

of which multiple | -0.5% | 0.2% |

Volatility of Total Return | 11.9% | 15.8% |

Volatility of growth | 1.9% | 11.3% |

Volatility of multiple | 10.9% | 13.8% |

Source: AMP Capital, Bloomberg. Data from 31 December 2007 to 31 March 2020. Data frequency: quarterly. Data period: Q1 2006 to Q1 2020. Currency: local. Global equities represented by MSCI World Index. Past performance is not a reliable indicator of future performance.

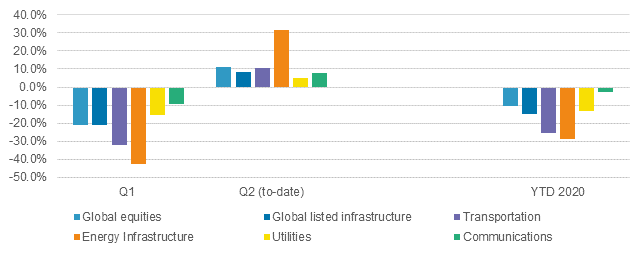

When global sharemarkets corrected due to the COVID-19 pandemic during the first quarter of 2020, listed infrastructure underperformed. The underperformance was primarily driven by the transportation and energy infrastructure sectors due to fears of COVID-19-led demand shock and OPEC+ driven oversupply.

The communications and utilities sectors outperformed as they benefited from a “flight to safety” market environment due to their defensive and long duration.

Figure 4: Performance comparison

Source: AMP Capital, Bloomberg at 30 April 2020. Data represented in USD. Global Equities represented by MSCI World Index. Past performance is not a reliable indicator of future performance.

The combination of the COVID-19 pandemic and the volatility in commodity prices presented a challenging environment for listed infrastructure.

However, when we look at the breakdown of the drawdown in the first quarter in figure 2 (above), the predominant driver was multiple compression (of valuations).

As we believe cash flow growth should be the key focus for long-term returns, the recent market dislocation (due to COVID-19) has caused attractive entry points within the asset class.

Outlook

Our long-term outlook for listed infrastructure remains positive, supported by a recovery in economic activity and industry-wide structural investment tailwinds.

While not all infrastructure sectors reacted in a defensive manner during the recent market downturn, we believe that an allocation to listed infrastructure provides diversification benefits to investors through the economic cycle.

We continue to see the potential for future outperformance as investors seek quality defensive assets that provide sustainable yield profiles in the current low interest rate environment.

Investors also need to be aware of risks specific to infrastructure investments such as regulatory and contractual risks and overall equity markets’ related risks, such as interest rate, commodity and share market investment risks.

About the author

ASX acknowledges the Traditional Owners of Country throughout Australia. We pay our respects to Elders past and present.

Artwork by: Lee Anne Hall, My Country, My People