Timings updated for mandatory climate disclosures

- Wed 26 June 2024

- 3 MIN READ

Some ASX entities have more time to get ready for the new reporting regime.

The Australian Accounting Standards Board (AASB) is currently finalising new sustainability reporting standards for local entities. Federal Treasury has wrapped up its consultation and the relevant legislation, Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Bill 2024 is going through parliament.

The AASB is presently finalising Exposure Draft ED SR1 Australian Sustainability Reporting Standards – Disclosure of Climate-related Financial Information. ED SR1 includes three draft Australian Sustainability Reporting Standards:

- ASRS 1 General Requirements for Disclosure of Climate-related Financial Information, developed using IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information.

- ASRS 2 Climate-related Financial Disclosures, developed using IFRS S2 Climate-related Disclosures as the baseline.

- ASRS 101 References in Australian Sustainability Reporting Standards.

AASB’s sustainability standards are designed to align with new International Sustainability Standards Board (ISSB) standards, with modifications for the Australian context. For example, they incorporate Australia’s national greenhouse gas emissions estimation methodologies and climate risk reporting requirements.

The ISSB has finalised sustainability and climate-related financial disclosure reporting standards to improve consistency and comparability across entities reporting around the world. The ISSB released IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures) in June 2023.

In Australia, climate-related financial disclosures will be mandated through amendments to the Corporations Act 2001 (Cth) and through the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Bill 2024.

The first group required to disclose information about climate-related risks and opportunities are large entities that prepare and lodge annual reports under Chapter 2M of the Corporations Act. This includes listed and unlisted companies.

"The ISSB has finalised sustainability and climate-related financial disclosure reporting standards to improve consistency and comparability across entities reporting around the world."

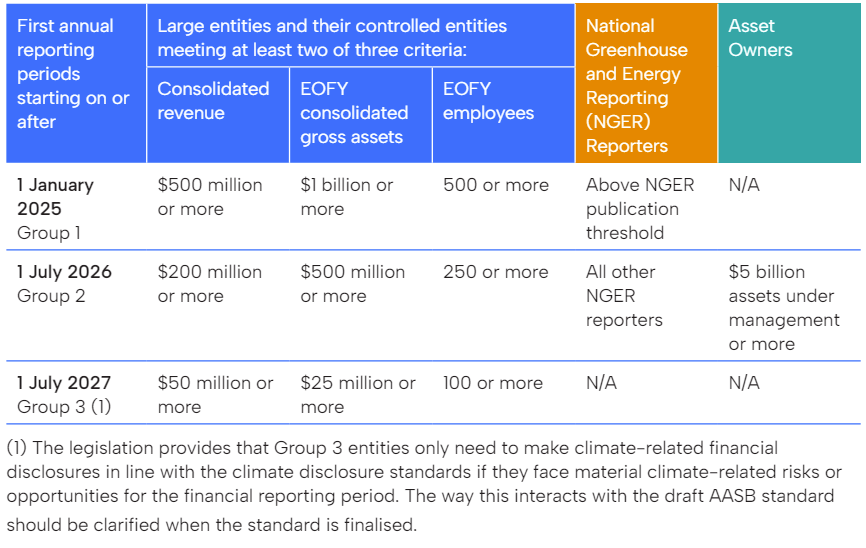

A reporting date of 1 January 2025 has been set for the first group of entities that need to comply with the new mandatory climate change reporting regulations. This is a 12-month extension for 20 June year-end reporters to the original 1 July 2024 commencement date, but there is no extension for entities with a calendar year end.

Below is a table that shows current reporting dates for the three categories of entities that are required to comply with the new reporting rules. There is a staggered, four-year approach to compliance, based on entity size and emission levels.

The table sets out when entities must start disclosing, assuming they prepare and lodge annual reports under Chapter 2M of the Corporations Act.

An entity will be required to disclose climate information regardless of size if it is subject to both the Corporations Act’s annual reporting requirements and the emissions-reporting obligations of the National Greenhouse and Energy Reporting Act 2007 (Cth).

A mandated climate reporting regime will deliver many benefits.

- Better climate disclosures published by Australian entities supports regulators to assess and manage systemic risks to the financial system as a result of climate change.

- A rigorous, internationally-aligned and credible climate disclosure regime will cement Australia’s reputation as an attractive destination for international capital and help draw the investment required for the transition to net zero.

- It heightens transparency over entities’ climate impacts for shareholders and supports efficient allocation of capital aligned with risks and opportunities.

About the reporting framework

Climate-related financial disclosures cover information about climate-related risks and opportunities, governance, strategy, risk management and metrics and targets, including Scope 1 and Scope 2 greenhouse gas emissions. Scope 3 emissions related to the supply chain and emissions associated with financing or investment activities will be required to be reported from year two.

"A mandated climate reporting regime will deliver many benefits."

Climate-related financial disclosures will sit within the entity’s sustainability report, a new report now required by reporting entities. Its recommended entities include an index table within their annual report to help readers to easily navigate the climate disclosures.

“It is proposed climate disclosures will be subject to similar assurance requirements, which will be phased in, to those currently in the Corporations Act for financial reports. This means reporting entities will need to obtain an assurance report from their financial auditors. Requirements will be set out in a standard published by the Auditing and Assurance Standards Board (AUASB) that is currently under consultation,” says Terence Jeyaretnam, EY Climate Change and Sustainability Services, who sits on the AUASB.

There is some breathing space for the majority of Group 1 entities to comply with new mandatory reporting requirements, given most are 30 June year ends. But now’s the time for ASX-listed businesses to get on top of the new standards to ensure they meet their requirements in full and on time.

New Zealand-based ASX-listed entities

Because Australia has chosen the Corporations Act Chapter 2M reporting requirements as the mechanism to impose climate-related financial disclosures, only companies incorporated or formed in Australia (s285(2)) will be required to report under this regime.

New Zealand-incorporated companies listed on ASX will not have to report under the Australian CRFD regime regardless of whether they report under the NZ regime, which applies only to NZX-listed companies.

Related links

About the author