Resources and Tech lead charge for ASX IPOs

- Thu 15 October 2020

Markets continued to stabilise and recover in Q3 from their March lows, with the benchmark S&P/ASX 200 relatively flat over the quarter and now down only 11% year to date (YTD) (from a 32% fall as at the low on 23rd March), ahead of both London and Hong Kong however trailing the tech heavy US benchmarks, both of which have returned to the black YTD. The S&P/ASX All Technology Index (XTX) launched back in February continued its outperformance, and is largely tracking in line with the Nasdaq Composite Index. Volatility remained elevated over the quarter, with trading volumes by daily value up nearly 30% versus 2019 levels YTD however down around 18% from the extreme levels seen at the end of Q1.

This level of relative stability enabled global IPO activity to pick up again in Q3 after a relatively slow start to the year, up 169% on Q2 2020 by volume per Dealogic. Between Nasdaq and NYSE, there were 195 new listings, which represent 80% of their year to date volume however it is noteworthy that nearly 45% of these IPO transactions related to SPACs, which after relatively low levels of issuance since the GFC, have enjoyed a renaissance over the last couple of years, reaching over 100 transactions this year alone.

This positive sentiment was also reflected in Australia, where ASX welcomed 22 new listings this quarter, a significant increase on Q2 (+83%). Offer sizes are also on the rise, with 4 companies (LBY, AIM, 4DX, PLT) raising IPO proceeds greater than $50m. Resources was the most heavily featured sector, followed by technology businesses. New Zealand companies led the charge from across the ditch, with 3 Kiwi companies (ARX, LBY, NZO) joining the boards bringing the total to 60 ASX-listed New Zealand companies – our largest source of international listings. ASX has attracted 50 new listings calendar year-to-date, slightly behind the same period last year, but ahead on a financial year-to-date basis.

In terms of on the secondary offerings, ASX continued to see heightened levels of capital raises by listed companies, with over 115 companies tapping the market for a combined $2.9b in July followed up by a further $6.2b raised in August by over 100 companies. The largest raises during these months were Sydney Airport (SYD) at $2b, followed by IOOF Holdings (IFL) with $1.04b and Afterpay (APT) raising $786m. Between mid-March and August, ASX saw over 550 companies raise a combined $38.5b. September saw the pace and size of raises begin to taper off as the market passed through annual reporting season and started to turn its attention to a host of IPO candidates.

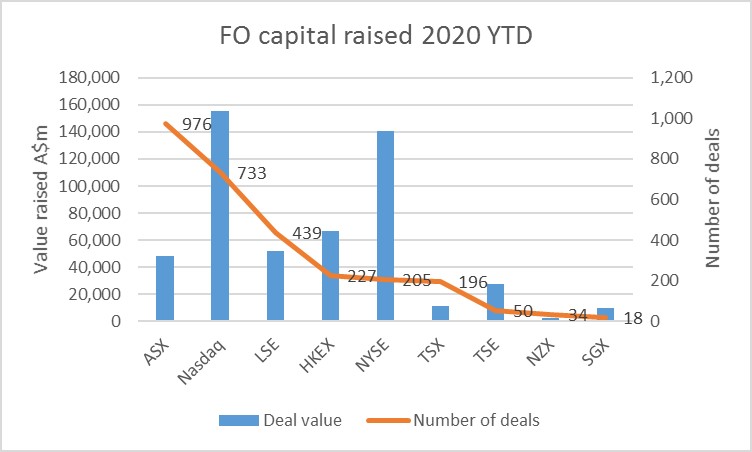

The Australian capital markets continue to punch well above its weight on a global basis, with ASX ranking 5th globally for total secondary capital raised, and is the leading exchange globally by number of follow-on capital raising events YTD, with nearly 1,000 raises per Dealogic – followed by Nasdaq, LSE, Hong Kong and NYSE.

Source: Dealogic 25th September 2020. Includes junior markets where applicable

The XTX had its second rebalance since it was launched earlier in the year, with 8 new companies admitted to the index. In the space of 7 months, the number of companies has increased from 46 to 58, and $40b added to the cumulative total market cap of the index.

What a difference a quarter can make in capital markets – secondary capital raisings have started to make way for IPOs with the window presently well and truly open. There are plenty of companies moving to line up an IPO prior to year-end, with heightened activity in junior resources and the technology space as well as a combination of companies dusting off deferred IPO plans from earlier in the year, the usual Q4 rush and those seeking to take advantage of current market conditions.

Notwithstanding the usual caveats around market conditions and a potentially divisive US election in November, it should be one of the busiest IPO seasons in some years here at ASX.

About the author

ASX acknowledges the Traditional Owners of Country throughout Australia. We pay our respects to Elders past and present.

Artwork by: Lee Anne Hall, My Country, My People