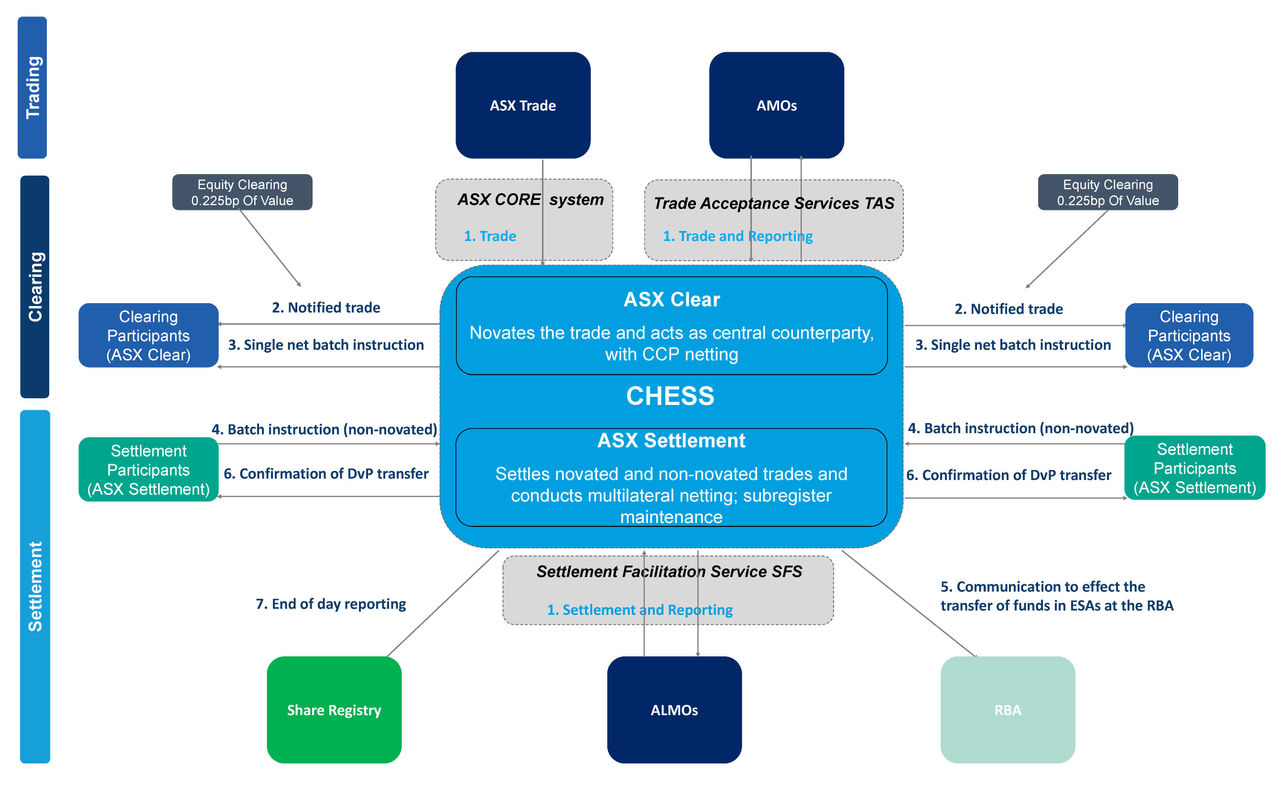

Clearing

The clearing of executed trades performs a critical role in the operation of Australia’s financial markets. ASX’s clearing services help reduce counterparty and systemic risk, and provide transaction efficiency and certainty for end investors.

The clearing process is largely invisible, but the benefits are shared by all financial market users.

Backed by significant capital and collateral, and overseen by Australian regulators, ASX's clearing infrastructure supports the world-class reputation of Australia's financial markets.