How to find dividends in 2021

- Fri 02 July 2021

Best yield results coming from non-traditional sources, such as resources, retailers.

Based on Plato’s analysis, 2020 was the worst year for dividends in Australia over the past 40 years. The 35% cut in dividends surpassed the falls seen over three years in the ‘recession we had to have' and the Global Financial Crisis.

For investors holding just bank shares, the outcome was even worse, with big-four bank dividends falling roughly 60% in calendar 2020. Self-funded retirees also took a huge hit on their interest income, with term deposit rates plunging to near zero.

But that was last year. We faced nationwide lockdowns, no one knew how bad things might get and many assumed the worst. The Reserve Bank of Australia slashed rates to an all-time low of 0.1%. The Australian Prudential Regulation Authority (APRA) initially discouraged banks from paying any dividends at all, and the Federal government literally threw money at Covid with its Jobkeeper and Jobseeker payments.

As we have seen, Australia’s island quarantine strategy has proved relatively successful, in fact highly successful in a global context. Our economy has bounced back quicker than anyone thought, and our GDP has now surpassed its pre-Covid levels.

For most companies, too, the outlook is bright, apart from those still directly affected by international travel bans and local lockdowns.

On our analysis, 2021 has emerged as a strong year for dividend income and with the August reporting season ahead, we expect the good news for dividend investors to continue into the remainder of the year.

The picture for income from ASX-listed equities is stark when compared to other asset classes. Below, we’ve charted the real earnings on $1 million from the overnight cash rate, 1-year term deposits, and 10-year bond yields. These so-called safe assets are producing negative real rates of return.

Source: Plato

So, in a world where real returns on cash-backed assets are in the red, and will likely remain there for the foreseeable future, how can investors ensure they don’t miss out on a piece of the dividend pie?

Dividend outlook promising

We model expected dividends for S&P/ASX 300 companies and our expectations for future dividends are looking bright. We also forecast the likelihood of companies potentially cutting their future dividends. This helps us avoid dividend traps, which we think is key for income investors.

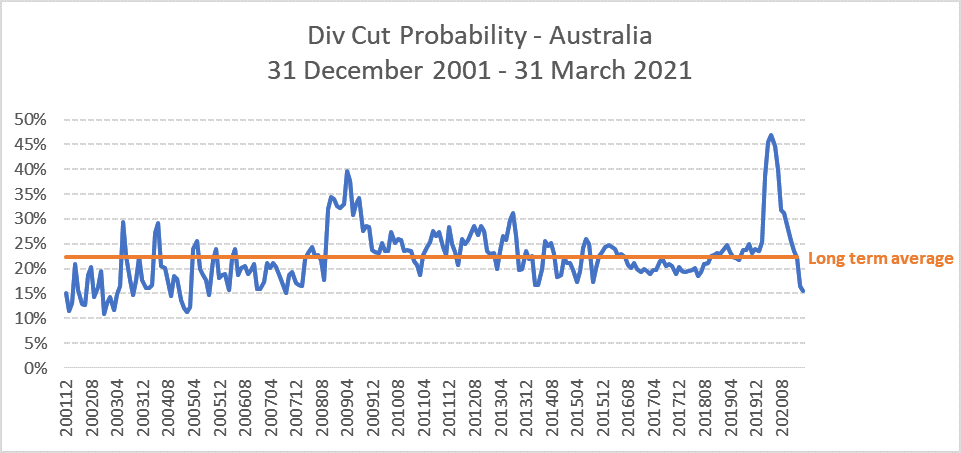

We can use our dividend-cut model to get a picture of the market as a whole, by calculating the average probability of a dividend cut across all stocks. The following chart shows how the probability has varied over time.

The GFC in 2008/9 and the Covid pandemic in 2020 are clear to see (in the chart below). The global pandemic set a new high for the market-wide probability of dividend cuts, but what is interesting is how quickly the cut probability has fallen from its peak in April 2020 to a below-average level. This underpins our positive outlook for dividends in 2021.

Source: Plato Global Dividend Cut Model

Diversify, but don’t set and forget

Plato manages the portfolio of its Listed Investment Company, the Plato Income Maximiser (ASX: PL8), with the aim of paying monthly dividends and delivering investors above-market levels of income annually. It may come as a surprise that the majority of our top-yielding holdings aren’t what many consider to be Australia’s traditional dividend-paying stocks.

(Editor’s note: Do not read the following ideas as stock recommendations. Do further research on your own or talk to a financial adviser before acting on themes in this article).

Consider the miners. Three of the top six dividend payers in Australia today are mining companies – Fortescue Metals Group (ASX: FMG), Rio Tinto (ASX: RIO), and BHP (ASX: BHP). For many investors, this would have been inconceivable just a few years ago.

We’ve held a positive view on the resources sector for several years, comfortable with the global supply/demand equation for iron ore. Over the past three years, FMG, RIO, and BHP alone have delivered our portfolio 3.4% per annum gross income.

The question we now face is how long will the mining-stock dividend boom continue?

We still maintain a positive outlook on mining-stock dividends for the foreseeable future. Our experience in active equity management has taught us things always take longer to play out than markets would indicate.

Samarco (the massive Brazilian Iron Ore miner owned by BHP and Vale) is only just coming back to full production five years after a devastating dam disaster. We often see miners forecast swift production resumption after major issues, but the reality is it usually takes longer. The Covid situation in Brazil is another impediment.

Even when this Brazilian supply comes back on, steel production is on the rise with historical levels of infrastructure stimulus leaving the supply-and-demand fundamentals intact. Should iron-ore prices come off $100-$150 per tonne from the current highs, Fortescue, Rio Tinto, and BHP will still be very profitable businesses.

Mining stocks go through cycles, and this fact shouldn’t be ignored. It’s why a “set and forget” approach isn’t optimal for dividend investing. We like miners for the short-medium term, but our view is likely to evolve as conditions change.

Retailer dividends

The same applies to retailers – again, not a traditional area for dividends in the eyes of income investors. However, it’s a sector that has produced exceptional income in recent times for investors who have actively added the right names to their portfolios.

In the consumer discretionary space, in particular, leading retailers, including JB Hi-Fi (ASX: JBH), Super Retail (ASX: SUL), and Harvey Norman Holdings (ASX: HVN), have been thriving and delivering income far superior to most other asset classes.

These consumer discretionary businesses (and others) experienced a Covid sugar-hit as consumers stocked up on products needed for working from home and increased domestic tourism, and we expect this to continue until borders are opened.

As active managers, we must consider if this will continue into the short-medium term.

It remains to be seen when full-scale international travel will resume. Australians love to travel and spend a lot of money abroad. A large chunk of that money is likely to continue flowing into domestic discretionary spending. There was evidence of this recently.

Bank dividends

When it comes to the big-four banks, they’ve traditionally been a major focus for income investors but in 2020 the outlook appeared dire as dividends were slashed across the board among the financials.

There has, however, been a remarkable turnaround, for three reasons. First, APRA took off all restrictions on bank and financial institution dividends in late 2020. Second, bad debts have proven much lower than expected. Finally, banks are seeing good loan growth fuelled by low interest rates.

In May, we saw half-year results from Westpac (ASX: WBC), ANZ (ASX: ANZ), and National Australia Bank (ASX: NAB).

Across the board, there has been a significant write-back of provisions and strong increases in cash earnings, resulting from improving economic conditions.

Outside of the big four, dividend strength is also evident. Bendigo and Adelaide Bank’s (ASX: BEN) half-year result earlier this year came in at almost 30% above expectations. Macquarie Group’s (ASX: MQG) FY21 net profit, revealed in May, was up 10% on FY20.

Although bank dividends aren’t fully back to pre-Covid levels, we believe the outlook is positive for the sector and think financials are once again an important element of a diverse equity income portfolio.

Individual dividend investors who set and forget can see their income plunge when the typical dividend stocks go through tough patches – such as the banks during the royal commission or the peak of the Covid crisis.

On the flip-side, we’re able to take a dynamic approach to generate high yield, moving around the market at any point to find strong dividends and capital returns.

Dividend income to make ends meet

In our low-rate world, effective dividend investing has been a shining light for income-seeking investors. With Australia seemingly through the worst of the Covid crisis, the outlook for dividends is improving.

Looking to the rest of 2021 and into 2022, we think there’s a positive outlook for dividends, particularly from ASX iron-ore miners, select consumer discretionary, and the banks.

Diversification, active management, and tax-effective investing can help fire up the dividend machine and ensure investors, who rely on their capital for income, don’t miss out.

About the author

The views, opinions or recommendations of the author in this article are solely those of the author and do not in any way reflect the views, opinions, recommendations, of ASX Limited ABN 98 008 624 691 and its related bodies corporate (“ASX”). ASX makes no representation or warranty with respect to the accuracy, completeness or currency of the content. The content is for educational purposes only and does not constitute financial advice. Independent advice should be obtained from an Australian financial services licensee before making investment decisions. To the extent permitted by law, ASX excludes all liability for any loss or damage arising in any way including by way of negligence.