Outlook for small-cap stocks, markets in 2021

- Fri 05 February 2021

ASX Investor Update asked three mFund members that have small-cap equity funds available via ASX, for their views.

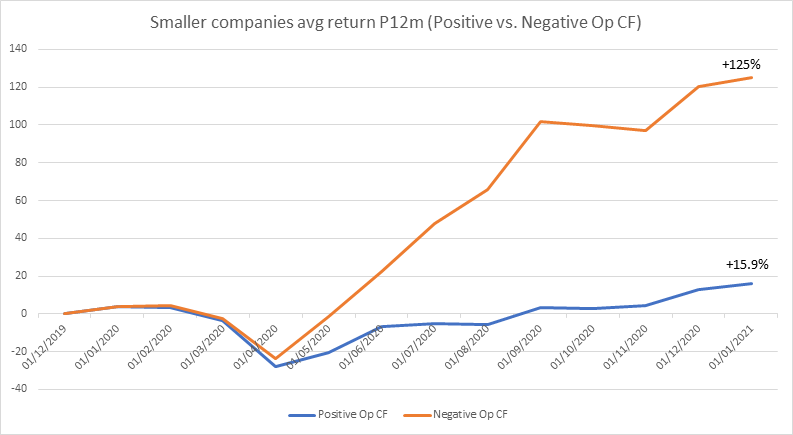

The ASX small-cap space today is characterised by a curious case of cash-flow distortion. A distortion that continues to see stocks that lose money outperform those that make money and have sound cash flow.

This is best illustrated in the chart below. You can see smaller companies that lose money at the operating cash-flow level (red line) returned an astronomical 125 per cent in the 12 months to January 12, 2021.

Positive operating cash-flow stocks (blue line) returned around 16 per cent during the same period.

If you were buying a small business to own and operate, would you pay more for one losing money than you would for one making money?

This topsy-turvy market epitomises what Benjamin Graham so eloquently wrote back in the 1930s – “In the short run, the market is a voting machine but in the long run it is a weighing machine.”

For the long-term investor who focuses on the weighing machine, this cash-flow distortion provides an abundance of opportunity.

Cash is key when investing in small caps. Yes, you might think this doesn’t ring true when looking at the chart above. But step back and it becomes clear that the weighing machine is far more powerful than the voting machine.

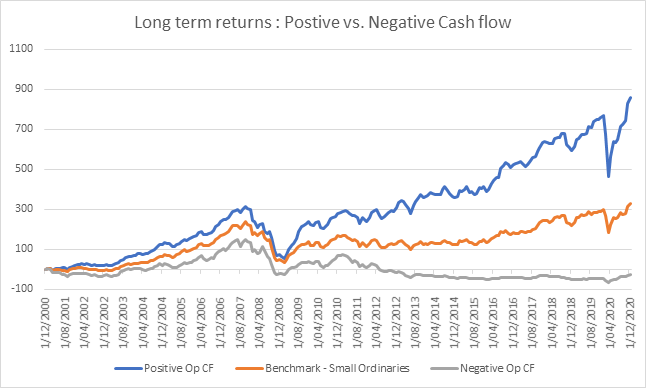

The Spheria team back-tested positive operating cash flow vs negative operating cash flow and the long-term outcome is stark.

In the chart below, the blue line (+860%) represents a bundle of all small-cap stocks with positive operating cash flow. The orange line (+325%) represents the index (a blend of positive and negative operating cash-flow stocks).

The grey line, in deeply negative territory, represents a portfolio of stocks with negative operating cash flow.

Chart Source: Bloomberg data: simple average return of stocks between $50m and 3.0bn market cap divided into positive op cash flow and negative op cash flow over prior 12 months.

Chart Source: Bloomberg data. Back-tested returns of stocks between $50m and 3.0bn market cap divided into positive op cash flow and negative op cash flow over the past 20 years.

Marcus Burns, Portfolio Manager, Spheria Asset Management

Our investment process is based on buying businesses that generate predictable free cash flows at an appropriate multiple for the forecast growth profile.

By default, this lends itself to screening out companies that don’t generate cash, lack sustainability or are being priced nonsensically by the market.

The cash-flow conversion rate is a key metric in this process and one of the most important characteristics for enduring small-cap returns.

To get a rate of cash-flow conversion, our team takes the reported EBIT (earnings before interest and tax) of a company, compares it to the free cash flow found in the company’s cash-flow statement and adjusts for CAPEX (capital expenditure) and interest.

(Editor’s note: Do not read the following ideas as share recommendations. Do further research of your own or talk to a licensed financial adviser before acting on themes in this article).

Through this lens, three smaller ASX companies that currently stand out to Spheria (to name a few) include Mortgage Choice ASX: MOC), A2B Australia (ASX: A2B)) and City Chic Collective (ASX: CCX)).

In recent months, many stocks with strong fundamentals that were ignored by the market for a lengthy period have been rewarded during the final quarter of 2020 and into the new year. These include Mortgage Choice, City Chic Collective, Seven West Media (ASX: SWM) and Supply Network (ASX: SNL).

But we believe the scales have further to go.

Cash burners are continuing to fly high as media and internet chat hype, along with the promise of “disruption”, rewards companies with negative cash flow. But history tells us over the long term the weighing machine scales do inevitably tip.

Those investors who focus on fundamentals will be rewarded, while the only thing most disruptors will disrupt is the greater fool’s bank balance.

So, what is the outlook for 2021? With an abundance of liquidity, extremely low interest rates and corporate confidence on the rise, we would anticipate more mergers & acquisitions (M&A) activity in the small- and micro-cap space.

In addition to private equity being in the fray, corporates now have extremely well-positioned balance sheets – with many having foregone paying dividends during most of calendar-year 2020 and some also having raised too much precautionary capital during the February/March COVID-related sell-off.

Most acquirers seek profitable, cash-generating companies with modest gearing to support their M&A rationale, which plays strongly to Spheria’s hand.

Principles to steer you through investment shoal

By Donny Buchanan, Lakehouse Capital

Investors beware: 2021 is filled with uncertainty!

Historically low interest rates, rising inflation risks, an appreciating Australian dollar, geopolitical and trade uncertainties among global superpowers, an out-of-control global pandemic, and market distortions from the greatest fiscal and monetary stimulus the world has ever seen are among the many dangers.

Predictions on these topics yield a low probability of real insight for most investors and little ability to control outcomes. Fortunately, there are some investing principles you can apply to tilt probabilities in your favour during these uncertain times.

First, put time on your side. There’s always something to worry about, and 2021 is no different. History has shown that despite economic recessions, depression, terrorist attacks, world wars, epidemics, pandemics, and much more, it has paid well to remain optimistic and maintain a long-term investment horizon.

According to analysis by Lakehouse Capital, since the inception of the S&P/ASX Small Ordinaries Accumulation Index over 20 years ago through to 31 December 2020, the index has yielded a positive return over a one -year holding period 67 per cent of the time.

Extending the holding period to three years increases the probability of positive returns to 68 per cent, five years to 78 per cent, and 10 years to 90 per cent.

Despite market gyrations, probabilities tell us you are likely best served by remaining invested in a well-diversified portfolio in the face of uncertainty.

Second, seek out businesses with strong positions in growing markets. Perhaps the most distinctive characteristic for this is recurrent, strong revenue growth.

A study by Boston Consulting Group and Morgan Stanley on the long-term drivers of investment returns for the S&P 500 from 1990-2009 highlighted that:

- over one year, revenue growth accounted for 29 per cent of investment returns

- over three years 50 per cent

- over 10 years a compelling 74 per cent

At Lakehouse, some of the opportunities we see in the early stages of long revenue growth trajectories include e-commerce, digital payments and cloud computing.

Third, align yourself alongside founder-led management teams. Numerous studies have revealed companies led by long-term founders yield superior results.

A 2012 publication by the Harvard Business Review (“What You Can Learn From Family Business”) concluded that founder-led businesses often outperform externally managed firms.

More recently, the Credit Suisse Research Institute found that since 2006, its proprietary universe of 1,000 “family-owned” companies outperformed “non-family-owned” companies by an annual average of 3.7 per cent.

The power of compounding means this outperformance is equivalent to a further doubling of a patient investor’s wealth over a 20-year time horizon. Fortunately, ASX has an abundance of founder-led small- cap companies to invest in.

Donny Buchanan, co-founder and senior analyst, Lakehouse Capital

Fourth, pay careful consideration to balance sheets. A leading cause of corporate, as well as personal, financial failure is excessive use of credit.

At Lakehouse, we pay careful attention to the financial positions of the small-cap companies in which we invest. Strong balance sheets offer optionality and allow companies to play offence when market or financial conditions inevitably turn, often to the detriment of financially stretched competitors.

Lastly, ensuring you pay a reasonable price in 2021 relative to the business’ prospects is paramount as it heavily tilts the odds of long-term outperformance in your favour.

While the uncertainties of 2021 may contrast with history, the fundamental investing principles of long-term investing should not.

Biden could put the brakes on

By Rory Hunter, SG Hiscock

Although SG Hiscock remains bullish on global equity markets over a 12-month period, we are cautious in the nearer term and feel the market is at, or reaching, a short-term high.

The catalyst for a move lower could be one of several things. While Democratic control of the US Senate has been viewed somewhat favourably by markets, mostly due to the expected sugar hit from a US$2 trillion stimulus package, the agenda that follows is likely to be less business friendly.

Once the market looks past the stimulus and towards President Biden’s proposed corporate tax and minimum wage hikes, growth rates are bound to be called into question as profit margins drift lower.

Layer on top of this the prospect of a near-term pick-up in global consumer price inflation and the prospect of a more meaningful correction in equity markets appears likely.

One of our favoured leading indicators of global inflation is the performance of emerging-market equities relative to emerging-market bonds, and we view a strong recent uptrend as being consistent with an imminent pickup in global consumer price inflation.

So, what does this mean and how are we thinking about positioning? A pickup in global consumer price inflation would likely result in a spike in sovereign bond yields and, concurrently, a move lower in global equity markets.

Long-duration equity exposures such as technology and healthcare (particularly medical devices and biopharma) would likely lead the market lower as discount rates move higher with sovereign yields. Concurrently, cyclical, value and resources exposures would likely remain more robust.

We view the above scenario as an opportunity to trim our cyclical exposures and move to overweight positions in tech and healthcare.

Given the US economy operates with flexible exchange rates, is a relatively open economy with respect to trade and is already highly indebted, fiscal expenditures have a net negative multiplier.

It is, therefore, our view that any spike in US consumer price inflation and the accompanied uptick in sovereign yields will be short lived.

We believe a secular inflation cycle is not at hand and that this uptick in yields is likely to represent a near-term high, thus offering investors the opportunity to position themselves for a return of the bull run in US Treasuries.

Adding weight to this thesis are the indications that consumer prices are being inflated by short-term factors including supply chain disruptions, national security concerns and a move away from just-in-time inventory.

Given our leaning towards a “quality growth” investment style, it has been our preference to expose the portfolio to the recovery trade via resources exposures rather than seeking short-term opportunities in the travel and consumer discretionary sectors.

In line with the expectation of a transitory inflation impulse, we also remain cognisant of the weak seasonal period the ASX Small Resources Index enters towards the end of April and will most likely use the window prior to this as an opportunity to trim our exposure.

Rory Hunter is an assistant portfolio manager, SG Hiscock

With an eye on the next 12 months, from a thematic perspective, a pandemic-related economic relapse will likely shift investors’ attention back to pockets of the market deemed to be positively disposed to the pandemic.

More contagious COVID strains spreading from the UK, South Africa and Brazil mean a higher proportion of country populations will need to be vaccinated to achieve herd immunity.

Technological adoption and innovation will likely continue at pace, and the prospect of tech regulation by the Biden administration seems overplayed. The pandemic has exposed flaws in the global healthcare system and there is now a widely held belief that we cannot afford to continue to reactively apply band-aids.

Medical care contributes only 20 per cent of positive health outcomes and there will need to be a shift of focus towards proactive, preventative measures. This will continue to drive innovation in diagnostics and medical technology.

About the author